Comments

No comments yet. You can be the first!

Most popular documents in this category

Content extract

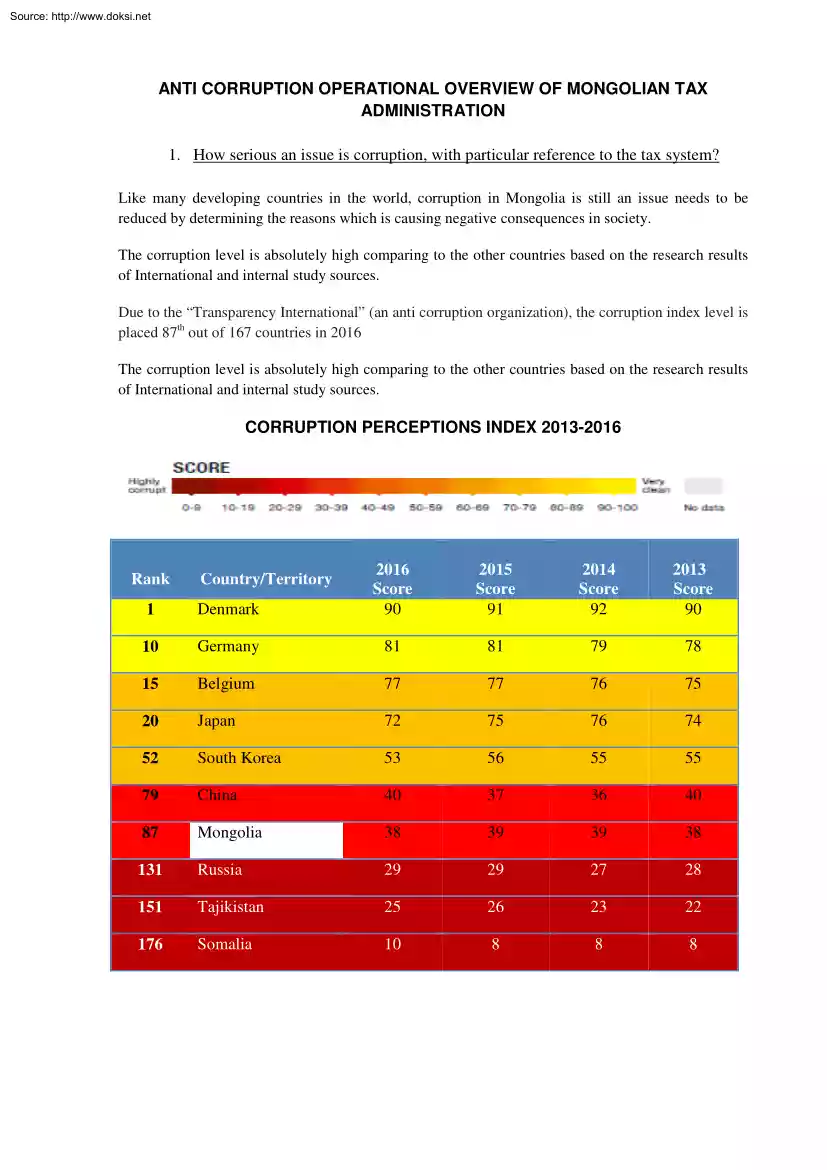

Source: http://www.doksinet ANTI CORRUPTION OPERATIONAL OVERVIEW OF MONGOLIAN TAX ADMINISTRATION 1. How serious an issue is corruption, with particular reference to the tax system? Like many developing countries in the world, corruption in Mongolia is still an issue needs to be reduced by determining the reasons which is causing negative consequences in society. The corruption level is absolutely high comparing to the other countries based on the research results of International and internal study sources. Due to the “Transparency International” (an anti corruption organization), the corruption index level is placed 87th out of 167 countries in 2016 The corruption level is absolutely high comparing to the other countries based on the research results of International and internal study sources. CORRUPTION PERCEPTIONS INDEX 2013-2016 1 Denmark 2016 Score 90 10 Germany 81 81 79 78 15 Belgium 77 77 76 75 20 Japan 72 75 76 74 52 South Korea 53 56 55 55 79

China 40 37 36 40 87 Mongolia 38 39 39 38 131 Russia 29 29 27 28 151 Tajikistan 25 26 23 22 176 Somalia 10 8 8 8 Rank Country/Territory 2015 Score 91 2014 Score 92 2013 Score 90 Source: http://www.doksinet However, according to the “Corruption index of Mongolia” informed by National Department Against Corruption shows that the number of corruption cases has been declined sligthly since year of 2012. Graph 1 Corruption index of Mongolia 1 140 120 100 80 60 40 20 0 1999 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 However, the results are different from the statistics of the official sources in the Corruption Sentiment Study in Mongolian Businesses and Public Perception Study on Corruption conducted among the business entities operating in Ulaanbaatar in October 2016 organized by Asia Foundation and Sant Maral Foundation. Participants in the Corruption Sentiment Study in Mongolian Businesses where CEOs and senior managers of 330

randomly selected Mongolian-owned companies were interviewed named the customs, tax, specialized inspection, court and police organizations as having higher corruption level among the state organizations. In 2016, Public Perception Study on Corruption was organized in Ulaanbaatar, aimags and soums covering 1,360 households. The study results showed the higher corruption level in Mongolia 1 http://www.iaacmn/old/pdf/surgalt/surgalt 2015 2pdf Source: http://www.doksinet Graph 2. Spread of Corruption in Mongolia Spread of Corruption, 2016 Political parties Offices in charge of land issues Mining Sector The Legislature / Parliament / Government Customs Government supply of local suppliers The court system Inspection Office Law enforcement authorities Health System Tax office Local governments Service for registration and license Education System Banks and other financial institutions 0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 According to the graph above, we can conclude that the Tax

Office is considered to be one of the highrisk corruption sectors among public institutions. 2. What forms does that corruption take? The activities to identify the forms of corruption are conducted by the Anti Corruption Agency in Mongolia. Subparagraph 1813 of the Anti Corruption Law stipulates that “conduct, at least once every two years, a survey on the scope, forms and causes of corruption, establish a corruption index, and inform the public.” The common forms of corruption are categorized in the following ways internationally: Bribes, Rewards, Gifts, and Abuse of Power. In our country, the last form or abuse of power has been evident recently to much extent for NGOs as illegal appointment of posts have been made numerously. 3. To what extent does the existing tax system help or hinder the removal of corruption? If we mention the following general causes for corruption in the state organizations: • • • • Low salary for state servants Challenges in business

environment Heavy bureaucracy Lack of adequate legal environment. We should mention the following causes for corruption depending the characteristics of the sector for tax organizations in addition to the above general causes: Source: http://www.doksinet • Procedure for grant of awards to state tax inspectors approved by the Government Resolution #344 of 2011 was not implemented after 2012 due to certain causes and there are not any other promotion systems for tax inspectors • The authorities of tax inspectors who conduct tax audits are set relatively higher in the frames of the relevant legislation • The monitoring system for the inspectors conducting tax audits is inadequate • Ethical control system for state tax inspectors is not elaborate and implementation of too general rules is unsatisfactory 4. What strategies are currently in place to combat corruption within the tax system? In 1996, anti corruption legal environment was created in our country and started to be

implemented officially. The State Great Khural of Mongolia has been implementing the following activities in order to create anti corruption legal environment and combat with corruption over the past years: • • • • • • 1996 Adoption of Anti Corruption Law 2002 Development of Anti Corruption National Programme 2005 Approval of U.N Anti Corruption Convention 2006 Revision of Anti Corruption Law 2007 Establishment of Anti Corruption Agency 2016 Adoption of Anti Corruption National Programme. Mongolia has been conducting anti corruption combat in all levels, and the General Department of Taxation is implementing the following activities within the framework of the Anti Corruption National Programme (hereinafter referred to as Programme) which is being implemented in order to fully keep the state away corruption and create business and competitive environment. Targets to strengthen fair, responsible and transparent public sector, and improve ethics: One key way to combat with

corruption crime is an action to change the common attitude of the people and illuminate them. Tax authority should pay more attention on creation of environment or condition which does not bear corrupted and bureaucratic state services among the taxpayers. In the direction of ensuring the openness and transparency of tax organizations, the following information of the employees should be registered, submitted to the relevant organizations, and stored in certain places: • • • Preliminary statement of personal interests of candidates for state services Personal interests statement for officials Income and asset statement for officials. In order to renew the methods and forms to asses, conclude and take accountability of the activities of the officials, Monitoring, evaluation, and assessment of the activities of tax authorities was renewed, approved and implemented in 2016. In the directions of Approval of model rules of public agencies, Analysis of ethical violations,

establishment and removal of causes and conditions, taking accountability, reporting and discussion: • National Tax Authority’s Ethics Rule approved by the Order #A/200 by the Commissioner of the General Department of Taxation in 2014 is now being followed. Source: http://www.doksinet • Ethics Commission with functions to ensure the implementation and control of the ethical rules of the National Tax Authority under the General Department of Taxation shall have 7 members while Ethics Commission under the aimag, capital city and district tax (divisions) departments will have an ethics commission with 3-5 members. Ensure the openness of state services, develop electronic services, improve quality and accessibility, respect interests of the customers, and increase the accountabilities of state servants: Within the framework of the objective to ensure the openness of state services and develop the electronic services, taxpayers’ registration, tax reports and attached

statistics of the reports, will be reported, received, tax payment registration, tax calculation registration, and tax debt accounting process will fully be computerized. Within the framework of the objective to conduct risk-based inspection and strengthen inspection, Risk-based Tax Inspection Plan was approved by the resolution of the Chairman of General Taxation Authority. The Plan is implemented on a monthly and quarterly basis As of 2016, 5215 inspections were planned within the frames of the above inspections and 5282 inspections were conducted with realization of the plan at 101.3% Statistics of the risk-based tax inspections are placed on Inspection Submenu of the Transparency Menu on www.mtamn, the website of the General Taxation Authority Within an objective for operation of transparent and open channel for claims and information, issuance and solution of claims and information by online, and create conditions for monitoring, advice is given to legal entities or organizations,

and individuals regarding the legislation and its implementation by phone, electronic way and in person. Also, taxpayers’ questions are being answered and their claims and requests are being received. This system is implemented by Tax Services Center upon its establishment. As of 2016, the number of taxpayers being served by the Center was 150,562, out of which 3827 claims were received and 3374 were solved. There were 35 requests to improve the operations of the tax organizations. Within the framework of improving the procurement control, responsibility and efficiency: Within an objective to introduce full electronic way in the tender activities, Consolidated Electronic Procurement System was introduced in order to make the procurement activities of the Government of Mongolia open and transparent, and improve the control on them. The General Taxation Authority is fully covered under the system starting from 2017, and procurement goods and services are fully transferred to electronic

tenders. 5. How effective are those strategies? As reported by the Independent National Department Against Corruption, there were 340 public servants inspected in relation to corruption in 2016. As a result of the measures implemented in relation to alleviation of corruption and combat with corruption by the tax authority, there were no cases where tax inspectors were found guilty in relation to corruption crimes at the court in 2016. 6. Are there other policies or strategies that could be adopted to help eradicate or mitigate corrupt activities? General Department of Taxation as an implementing agency of the Government, will have an obligation to ensure the implementation of the National Anti Corruption Programme in the future and is planning to conduct the following activities: Source: http://www.doksinet Clause 4.17 of the Programme Within an objective to support the initiatives of the civil society organizations: In order to ensure the citizens’ and public control on the

state organizations and their management, Subcommittee for Public Monitoring was established under the General Department of Taxation with the involvement of independent institutions with the purpose of prevention of tax inspectors from corruption. The subcommittee will operate in the following fields: increase involvement of the citizens and public in the corruption prevention activities, monitoring of the activities of the tax organizations and ethics of the tax inspectors, control accurate and legal income and asset reporting by the public officials. We are now studying the possibilities and conditions for implementation of internationally-known “Whistle Blower” system where interests of the reporter and critics on the corruption issues are protected. Mongolia introduced Corruption Barometer Study as conducted by “Transparency International” among 17 Asian countries. In the study, Mongolia is advised to create a legal environment for the protection of interests of whistle

blowers. The understanding should not be implemented not only nationwide, but also organization wide. A system to protect those who protests the improper acts inside the organization, fraud, corruption and briberies

China 40 37 36 40 87 Mongolia 38 39 39 38 131 Russia 29 29 27 28 151 Tajikistan 25 26 23 22 176 Somalia 10 8 8 8 Rank Country/Territory 2015 Score 91 2014 Score 92 2013 Score 90 Source: http://www.doksinet However, according to the “Corruption index of Mongolia” informed by National Department Against Corruption shows that the number of corruption cases has been declined sligthly since year of 2012. Graph 1 Corruption index of Mongolia 1 140 120 100 80 60 40 20 0 1999 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 However, the results are different from the statistics of the official sources in the Corruption Sentiment Study in Mongolian Businesses and Public Perception Study on Corruption conducted among the business entities operating in Ulaanbaatar in October 2016 organized by Asia Foundation and Sant Maral Foundation. Participants in the Corruption Sentiment Study in Mongolian Businesses where CEOs and senior managers of 330

randomly selected Mongolian-owned companies were interviewed named the customs, tax, specialized inspection, court and police organizations as having higher corruption level among the state organizations. In 2016, Public Perception Study on Corruption was organized in Ulaanbaatar, aimags and soums covering 1,360 households. The study results showed the higher corruption level in Mongolia 1 http://www.iaacmn/old/pdf/surgalt/surgalt 2015 2pdf Source: http://www.doksinet Graph 2. Spread of Corruption in Mongolia Spread of Corruption, 2016 Political parties Offices in charge of land issues Mining Sector The Legislature / Parliament / Government Customs Government supply of local suppliers The court system Inspection Office Law enforcement authorities Health System Tax office Local governments Service for registration and license Education System Banks and other financial institutions 0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 According to the graph above, we can conclude that the Tax

Office is considered to be one of the highrisk corruption sectors among public institutions. 2. What forms does that corruption take? The activities to identify the forms of corruption are conducted by the Anti Corruption Agency in Mongolia. Subparagraph 1813 of the Anti Corruption Law stipulates that “conduct, at least once every two years, a survey on the scope, forms and causes of corruption, establish a corruption index, and inform the public.” The common forms of corruption are categorized in the following ways internationally: Bribes, Rewards, Gifts, and Abuse of Power. In our country, the last form or abuse of power has been evident recently to much extent for NGOs as illegal appointment of posts have been made numerously. 3. To what extent does the existing tax system help or hinder the removal of corruption? If we mention the following general causes for corruption in the state organizations: • • • • Low salary for state servants Challenges in business

environment Heavy bureaucracy Lack of adequate legal environment. We should mention the following causes for corruption depending the characteristics of the sector for tax organizations in addition to the above general causes: Source: http://www.doksinet • Procedure for grant of awards to state tax inspectors approved by the Government Resolution #344 of 2011 was not implemented after 2012 due to certain causes and there are not any other promotion systems for tax inspectors • The authorities of tax inspectors who conduct tax audits are set relatively higher in the frames of the relevant legislation • The monitoring system for the inspectors conducting tax audits is inadequate • Ethical control system for state tax inspectors is not elaborate and implementation of too general rules is unsatisfactory 4. What strategies are currently in place to combat corruption within the tax system? In 1996, anti corruption legal environment was created in our country and started to be

implemented officially. The State Great Khural of Mongolia has been implementing the following activities in order to create anti corruption legal environment and combat with corruption over the past years: • • • • • • 1996 Adoption of Anti Corruption Law 2002 Development of Anti Corruption National Programme 2005 Approval of U.N Anti Corruption Convention 2006 Revision of Anti Corruption Law 2007 Establishment of Anti Corruption Agency 2016 Adoption of Anti Corruption National Programme. Mongolia has been conducting anti corruption combat in all levels, and the General Department of Taxation is implementing the following activities within the framework of the Anti Corruption National Programme (hereinafter referred to as Programme) which is being implemented in order to fully keep the state away corruption and create business and competitive environment. Targets to strengthen fair, responsible and transparent public sector, and improve ethics: One key way to combat with

corruption crime is an action to change the common attitude of the people and illuminate them. Tax authority should pay more attention on creation of environment or condition which does not bear corrupted and bureaucratic state services among the taxpayers. In the direction of ensuring the openness and transparency of tax organizations, the following information of the employees should be registered, submitted to the relevant organizations, and stored in certain places: • • • Preliminary statement of personal interests of candidates for state services Personal interests statement for officials Income and asset statement for officials. In order to renew the methods and forms to asses, conclude and take accountability of the activities of the officials, Monitoring, evaluation, and assessment of the activities of tax authorities was renewed, approved and implemented in 2016. In the directions of Approval of model rules of public agencies, Analysis of ethical violations,

establishment and removal of causes and conditions, taking accountability, reporting and discussion: • National Tax Authority’s Ethics Rule approved by the Order #A/200 by the Commissioner of the General Department of Taxation in 2014 is now being followed. Source: http://www.doksinet • Ethics Commission with functions to ensure the implementation and control of the ethical rules of the National Tax Authority under the General Department of Taxation shall have 7 members while Ethics Commission under the aimag, capital city and district tax (divisions) departments will have an ethics commission with 3-5 members. Ensure the openness of state services, develop electronic services, improve quality and accessibility, respect interests of the customers, and increase the accountabilities of state servants: Within the framework of the objective to ensure the openness of state services and develop the electronic services, taxpayers’ registration, tax reports and attached

statistics of the reports, will be reported, received, tax payment registration, tax calculation registration, and tax debt accounting process will fully be computerized. Within the framework of the objective to conduct risk-based inspection and strengthen inspection, Risk-based Tax Inspection Plan was approved by the resolution of the Chairman of General Taxation Authority. The Plan is implemented on a monthly and quarterly basis As of 2016, 5215 inspections were planned within the frames of the above inspections and 5282 inspections were conducted with realization of the plan at 101.3% Statistics of the risk-based tax inspections are placed on Inspection Submenu of the Transparency Menu on www.mtamn, the website of the General Taxation Authority Within an objective for operation of transparent and open channel for claims and information, issuance and solution of claims and information by online, and create conditions for monitoring, advice is given to legal entities or organizations,

and individuals regarding the legislation and its implementation by phone, electronic way and in person. Also, taxpayers’ questions are being answered and their claims and requests are being received. This system is implemented by Tax Services Center upon its establishment. As of 2016, the number of taxpayers being served by the Center was 150,562, out of which 3827 claims were received and 3374 were solved. There were 35 requests to improve the operations of the tax organizations. Within the framework of improving the procurement control, responsibility and efficiency: Within an objective to introduce full electronic way in the tender activities, Consolidated Electronic Procurement System was introduced in order to make the procurement activities of the Government of Mongolia open and transparent, and improve the control on them. The General Taxation Authority is fully covered under the system starting from 2017, and procurement goods and services are fully transferred to electronic

tenders. 5. How effective are those strategies? As reported by the Independent National Department Against Corruption, there were 340 public servants inspected in relation to corruption in 2016. As a result of the measures implemented in relation to alleviation of corruption and combat with corruption by the tax authority, there were no cases where tax inspectors were found guilty in relation to corruption crimes at the court in 2016. 6. Are there other policies or strategies that could be adopted to help eradicate or mitigate corrupt activities? General Department of Taxation as an implementing agency of the Government, will have an obligation to ensure the implementation of the National Anti Corruption Programme in the future and is planning to conduct the following activities: Source: http://www.doksinet Clause 4.17 of the Programme Within an objective to support the initiatives of the civil society organizations: In order to ensure the citizens’ and public control on the

state organizations and their management, Subcommittee for Public Monitoring was established under the General Department of Taxation with the involvement of independent institutions with the purpose of prevention of tax inspectors from corruption. The subcommittee will operate in the following fields: increase involvement of the citizens and public in the corruption prevention activities, monitoring of the activities of the tax organizations and ethics of the tax inspectors, control accurate and legal income and asset reporting by the public officials. We are now studying the possibilities and conditions for implementation of internationally-known “Whistle Blower” system where interests of the reporter and critics on the corruption issues are protected. Mongolia introduced Corruption Barometer Study as conducted by “Transparency International” among 17 Asian countries. In the study, Mongolia is advised to create a legal environment for the protection of interests of whistle

blowers. The understanding should not be implemented not only nationwide, but also organization wide. A system to protect those who protests the improper acts inside the organization, fraud, corruption and briberies

When reading, most of us just let a story wash over us, getting lost in the world of the book rather than paying attention to the individual elements of the plot or writing. However, in English class, our teachers ask us to look at the mechanics of the writing.

When reading, most of us just let a story wash over us, getting lost in the world of the book rather than paying attention to the individual elements of the plot or writing. However, in English class, our teachers ask us to look at the mechanics of the writing.